Markets Insights & Strategy

Asset Strategy Intelligence

- Annual Returns 20-50% with Zero Market Correlation: The Asset Class Wall Street Doesn’t Want You to Know About

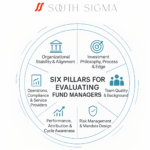

- Evaluating External Fund Managers in 2025

- How Private Credit Funds Are Delivering 11% Returns While Bonds Struggle

- Life Settlement Funds: A Comprehensive Investment Guide for Institutional and Sophisticated Investors

Research South Sigma Disclaimer

South Sigma Consulting FZCO (“South Sigma”) is an independent investment research and advisory firm providing consulting services to advisory groups, family offices, and institutional investors. Our services include manager sourcing, strategy due diligence, and portfolio design, with a focus on alternative investments such as hedge funds, private markets, real assets, and infrastructure. The information provided by South Sigma is intended solely for sophisticated and professional investors and is for informational and discussion purposes only. It is not intended for retail investors or the general public. South Sigma does not provide financial product advice, nor does it offer, promote, or distribute specific investment products or securities. All research, opinions, and assessments are provided on a non-reliance basis and should not be interpreted as a recommendation to invest, hold, or divest from any particular fund, manager, or strategy. Users are solely responsible for verifying the information provided and conducting their own due diligence. Investment decisions should be made based on independent judgment and, where appropriate, in consultation with qualified financial, legal, and tax advisors. While South Sigma strives to ensure the accuracy and reliability of the information it provides, no warranty or representation is made as to its completeness, accuracy, or fitness for any particular purpose. The information is provided “as is,” and South Sigma disclaims all warranties, express or implied, including but not limited to warranties of merchantability and fitness for a particular purpose. South Sigma does not act as a fiduciary or agent for any party and accepts no liability for any loss arising directly or indirectly from the use of information provided in the course of its consulting services. The information is not a substitute for professional advice. All content is confidential and proprietary to South Sigma Consulting FZCO. It may not be reproduced, distributed, or published without prior written consent from South Sigma.

For inquiries, please contact info@southsigma.com.