How Private Credit Funds Are Delivering 11% Returns While Bonds Struggle

Private Credit Funds: The Complete Investment Guide

Key Takeaways:

Superior Returns: Private credit has delivered 9.3% annualized returns over the past decade, significantly outperforming high yield bonds (5.9%), leveraged loans (4.4%), and investment grade bonds (3.7%).

Market Expansion: The private credit market has grown from $750 billion in 2018 to nearly $2 trillion in 2024, with projections indicating continued expansion.

Risk Management: Private credit demonstrates superior risk-adjusted returns with a Sharpe ratio of 2.61, compared to 0.54 for high yield bonds and 0.45 for leveraged loans.

Diversification Benefits: Private credit exhibits low correlation with traditional asset classes (0.39 with equities, -0.02 with investment grade bonds), providing excellent portfolio diversification.

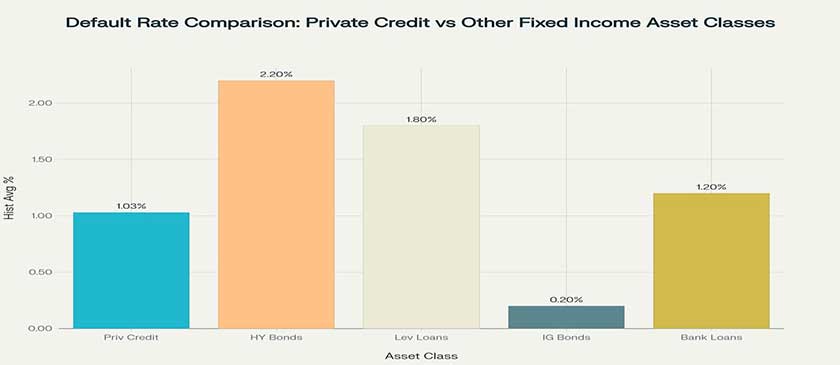

Credit Quality: Historical default rates of 1.03% are significantly lower than high yield bonds (2.2%) and competitive with leveraged loans (1.8%), while offering superior recovery rates of 68%.

Resilience: Private credit demonstrated remarkable stability during market stress, experiencing only 1.1% losses during COVID-19 compared to 2.2% for high yield bonds.

Executive Summary

Private credit has emerged as one of the most compelling alternative investment opportunities for institutional and sophisticated investors, representing a fundamental shift in how credit is allocated in modern capital markets. This comprehensive guide examines private credit as an asset class, analyzing its performance characteristics, risk profile, and strategic role in diversified investment portfolios with enhanced historical data and comparative analysis.

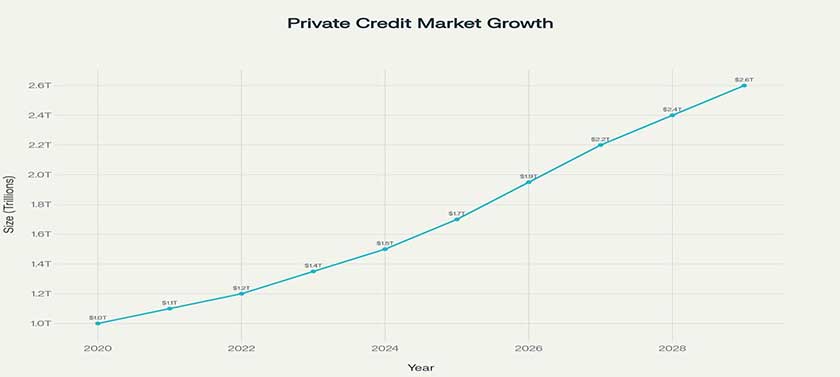

The asset class has demonstrated remarkable growth, expanding from $1.0 trillion in 2020 to $1.5 trillion in 2024, with projections indicating continued expansion to $2.6 trillion by 2029. Historical performance data shows private credit has generated net returns averaging 8-12% annually while maintaining relatively low correlations with public markets, making it an attractive complement to traditional asset classes.

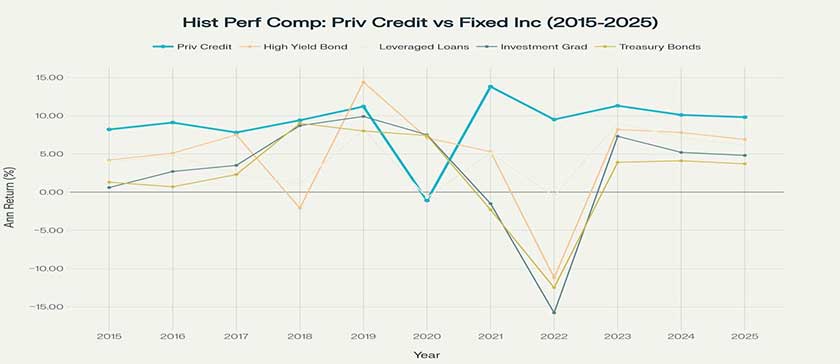

Historical performance comparison showing private credit’s superior and more consistent returns compared to other fixed income asset classes over the past decade.

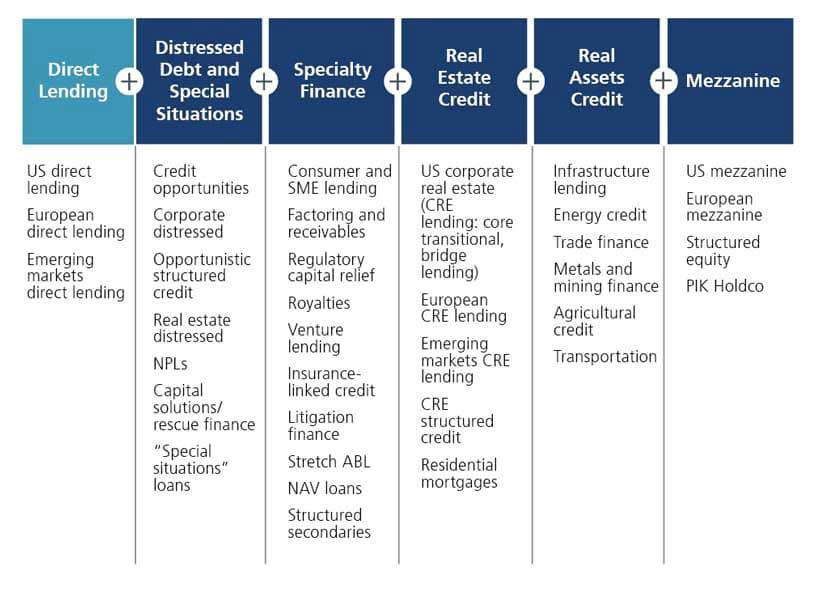

Overview of various private credit categories, including direct lending, distressed debt, specialty finance, real estate credit, real assets credit, and mezzanine.

Introduction to Private Credit as an Asset Class

Private credit represents non-bank lending to companies that are typically too large for traditional bank financing but too small for public bond markets. Unlike public credit markets where banks follow an originate-and-distribute model, private credit managers maintain ongoing relationships with borrowers, providing customized financing solutions with enhanced protective covenants.

This relationship-driven approach creates several key advantages: greater transparency into borrower operations, stronger alignment between lenders and investors, and superior downside protection through comprehensive covenant packages. The asset class encompasses several distinct strategies, including direct lending, mezzanine financing, distressed credit, and specialty finance.

Direct lending, which represents the largest segment, involves providing senior secured loans to middle-market companies, typically in conjunction with private equity transactions. These loans generally feature floating rate structures with spread over SOFR, providing natural inflation protection and interest rate sensitivity benefits.

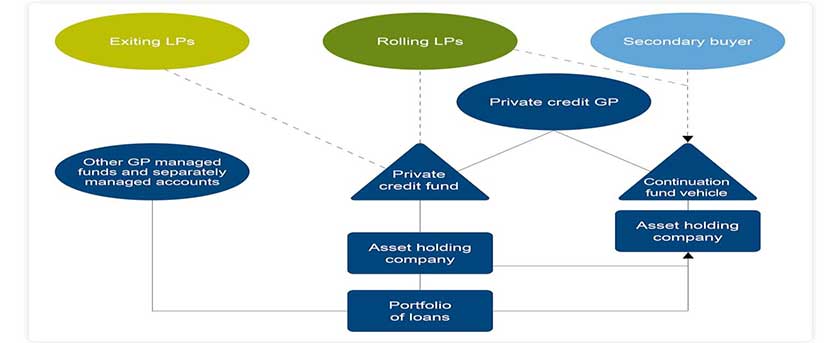

Flowchart illustrating the structure and process of private credit continuation funds and direct lending investments.

Historical Performance Analysis and Comparative Returns

Private credit has delivered compelling risk-adjusted returns across multiple market cycles, significantly outperforming traditional fixed income alternatives. Recent data shows private credit closed-end funds posted a 6.9% annual return in 2024, continuing their multi-year outperformance streak.

The Cliffwater Direct Lending Index (CDLI) achieved an 11.3% return in 2024 and a 9.3% annualized return from 2005-2022, compared to just 4.4% for leveraged loans and 5.9% for high yield bonds over the same period. This performance advantage becomes even more pronounced when examining different time horizons, with private credit demonstrating consistent positive vintage year IRRs, with median returns of approximately 8% for funds launched between 2010-2019.

Private credit’s superior risk-adjusted returns are evidenced by its Sharpe ratio of 2.61 compared to 0.45 for leveraged loans and 0.54 for high yield bonds. The asset class has also demonstrated remarkable resilience during market stress, with direct lending experiencing only 1.1% losses during the COVID-19 pandemic compared to 2.2% for high yield bonds and 1.3% for leveraged loans.

Long-term Average Annual Returns: Private Credit vs Other Asset Classes

Private credit’s superior risk-adjusted returns are evidenced by its Sharpe ratio of 2.61 compared to 0.45 for leveraged loans and 0.54 for high yield bonds. The asset class has also demonstrated remarkable resilience during market stress, with direct lending experiencing only 1.1% losses during the COVID-19 pandemic compared to 2.2% for high yield bonds and 1.3% for leveraged loans.

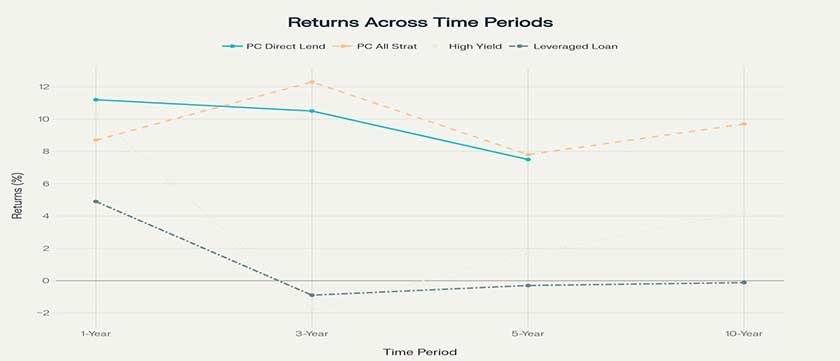

Private Credit vs Fixed Income Performance Across Time Horizons

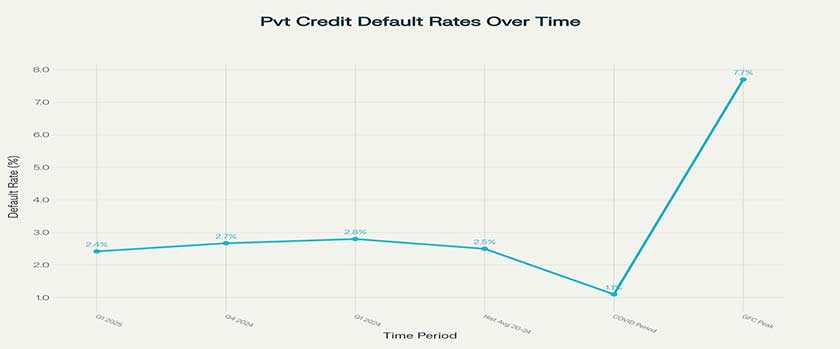

Historical Private Credit Default Rates Across Different Market Periods

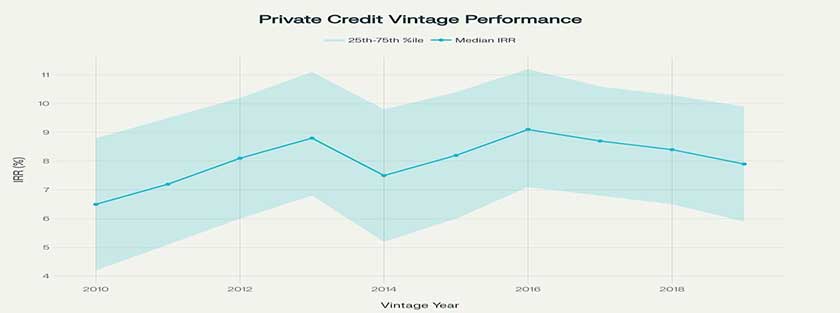

Vintage Year Performance Consistency

Historical analysis reveals that private credit has achieved positive returns in every vintage year over the past 23 years, demonstrating exceptional consistency across market cycles. The performance distribution shows relatively tight bands around median returns, indicating lower dispersion compared to other private markets strategies.

Private Credit Vintage Year Performance (2010-2019): Median IRR with Interquartile Range

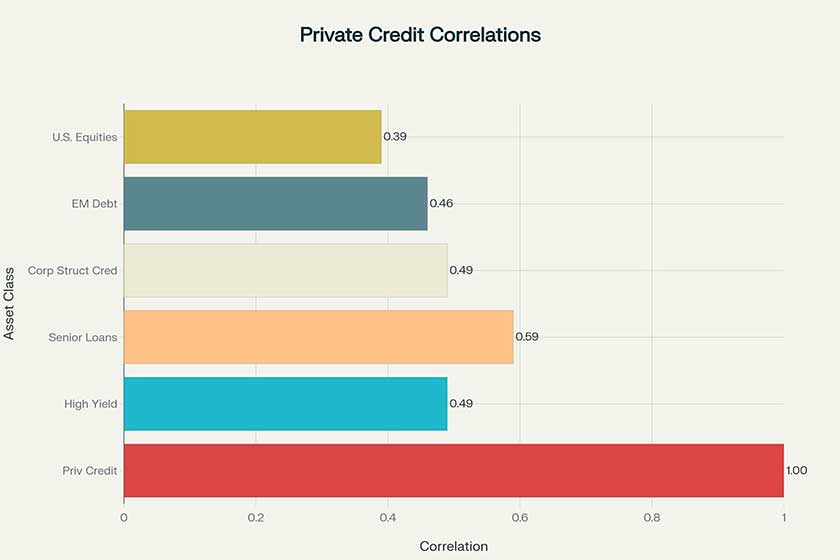

Portfolio Diversification and Correlation Benefits

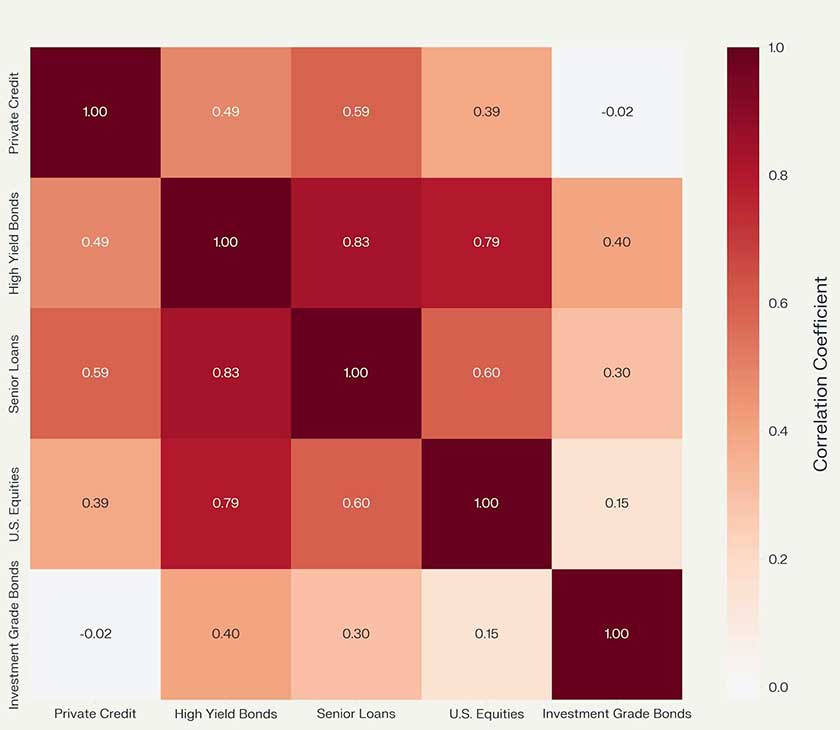

Private credit provides significant diversification benefits due to its low correlation with traditional asset classes. Correlation analysis demonstrates that private credit exhibits a correlation of only 0.39 with U.S. equities, 0.49 with high yield bonds, and 0.59 with senior loans. Most notably, private credit shows a negative correlation of -0.02 with investment grade bonds, providing excellent diversification within fixed income allocations.

Correlation heatmap

This low correlation profile enables private credit to serve as an effective portfolio diversifier, potentially reducing overall portfolio volatility while enhancing risk-adjusted returns. The diversification benefits stem from several factors: private credit’s relationship-driven nature insulates it from market sentiment, the floating rate structure reduces sensitivity to interest rate changes, and the focus on middle-market companies provides exposure to less cyclical businesses.

Correlation Between Private Credit and Traditional Asset Classes

Vintage Year Performance Consistency

Historical analysis reveals that private credit has achieved positive returns in every vintage year over the past 23 years, demonstrating exceptional consistency across market cycles. The performance distribution shows relatively tight bands around median returns, indicating lower dispersion compared to other private markets strategies.

Market Size and Growth Trajectory

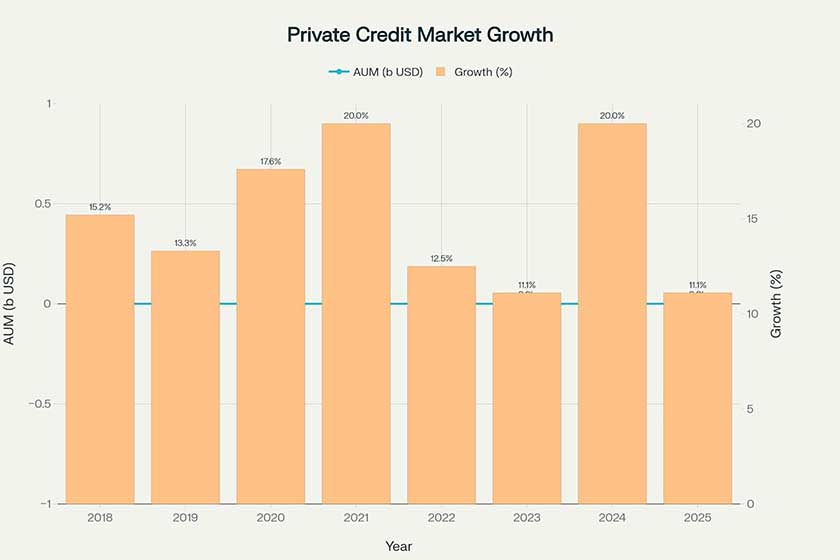

The private credit market has experienced unprecedented growth over the past decade, driven by regulatory constraints on traditional bank lending and increasing institutional investor demand for yield and diversification. The market expanded from $750 billion in 2018 to nearly $2 trillion in 2024, representing a compound annual growth rate of approximately 17%.

Private credit market expansion showing steady growth in assets under management from $750 billion in 2018 to projected $2 trillion in 2025.

Market expansion has been particularly pronounced in the United States and Europe, where regulatory frameworks have created favorable conditions for private credit growth. The Dodd-Frank Act and Basel III regulations have constrained traditional bank lending capacity, creating opportunities for private credit managers to fill the financing gap.

Supply and demand dynamics continue to favor private credit expansion, with private equity dry powder reaching record levels of $1.6 trillion in 2024, much of which requires debt financing for leveraged buyouts and growth capital transactions. Meanwhile, insurance companies and pension funds are increasing their allocations to private credit, seeking the illiquidity premium and enhanced yields the asset class provides.

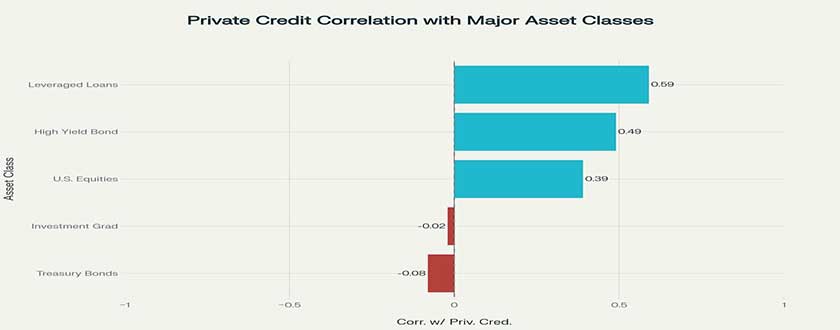

Portfolio Diversification and Correlation Benefits

Private credit provides significant diversification benefits due to its low correlation with traditional asset classes. Correlation analysis demonstrates that private credit exhibits a correlation of only 0.39 with U.S. equities, 0.49 with high yield bonds, and 0.59 with senior loans.

Most notably, private credit shows a negative correlation of -0.02 with investment grade bonds, providing excellent diversification within fixed income allocations. This low correlation profile enables private credit to serve as an effective portfolio diversifier, potentially reducing overall portfolio volatility while enhancing risk-adjusted returns.

Correlation analysis showing private credit’s low correlation with major asset classes, particularly negative correlation with government bonds, demonstrating excellent diversification potential.

The diversification benefits stem from several factors: private credit’s relationship-driven nature insulates it from market sentiment, the floating rate structure reduces sensitivity to interest rate changes, and the focus on middle-market companies provides exposure to less cyclical businesses. Additionally, private credit’s illiquid nature means valuations are less volatile than traded securities, contributing to smoother return profiles.

Risk Analysis and Default Rate Comparison

While private credit offers attractive return potential, investors must carefully evaluate and manage several key risk factors. Credit risk analysis reveals that private credit has historically maintained lower default rates and superior recovery rates compared to public credit markets.

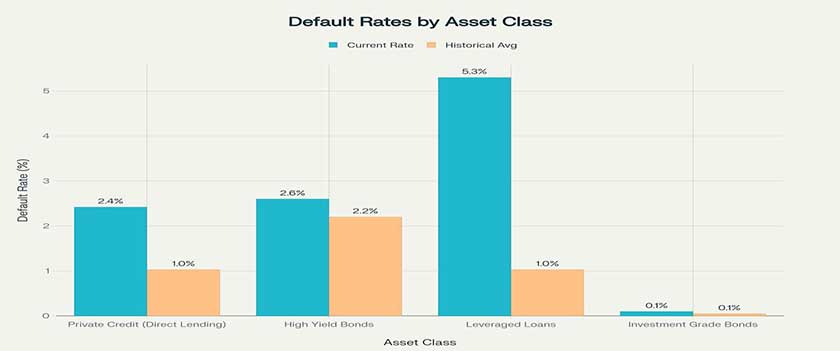

Current data shows private credit default rates of 2.42% for Q1 2025, which remains below the 5.3% default rate for leveraged loans and comparable to the 2.6% rate for high yield bonds. More importantly, the historical average loss rate for private credit stands at just 1.03%, significantly below the 2.2% historical loss rate for high yield bonds.

Default rate comparison showing private credit’s competitive credit performance with lower historical default rates than high yield bonds and leveraged loans.

Recovery rates further highlight private credit’s defensive characteristics, with infrastructure debt achieving 68% recovery rates compared to just 33.7% for unsecured high yield bonds. These superior recovery outcomes result from private credit’s collateral-backed structures and the direct relationships that enable proactive workout management.

Current Default Rates vs Historical Loss Rates: Private Credit and Other Fixed Income Assets

Recovery rates further highlight private credit’s defensive characteristics, with infrastructure debt achieving 68% recovery rates compared to just 33.7% for unsecured high yield bonds. These superior recovery outcomes result from private credit’s collateral-backed structures and the direct relationships that enable proactive workout management.

Credit Risk Management

Credit risk represents the primary concern for private credit investors, as these investments typically involve non-investment grade borrowers. Private credit managers employ sophisticated underwriting processes to evaluate borrower creditworthiness, including comprehensive financial analysis, management assessment, and industry evaluation.

Due diligence processes typically span 6-12 weeks and involve detailed review of financial statements, cash flow projections, competitive positioning, and management capabilities. Risk mitigation strategies include diversification across borrowers, industries, and geographies, as well as implementation of robust covenant packages that provide early warning indicators of borrower distress.

Liquidity Risk Considerations

Private credit investments are inherently illiquid, with typical hold periods of 3-7 years. This illiquidity creates both risks and opportunities: while investors cannot readily exit positions during market stress, they receive an illiquidity premium for accepting this constraint.

Insurance companies and pension funds, with their long-term liability profiles, are particularly well-suited to accept this illiquidity in exchange for enhanced yield. Leading managers maintain portfolio concentration limits, typically restricting individual position sizes to 2-5% of total fund assets.

Interest Rate and Market Risk

The floating rate nature of most private credit investments provides natural protection against interest rate increases. However, rapid rate increases can stress borrower cash flows, particularly for highly leveraged companies.

Leading managers monitor borrower interest coverage ratios and maintain detailed stress testing models to assess portfolio sensitivity to rate changes. The 2022-2023 rising rate environment provided another test of private credit’s defensive characteristics, with private credit funds generally generating positive returns due to their floating rate structures.

Performance Metrics and Risk-Adjusted Returns

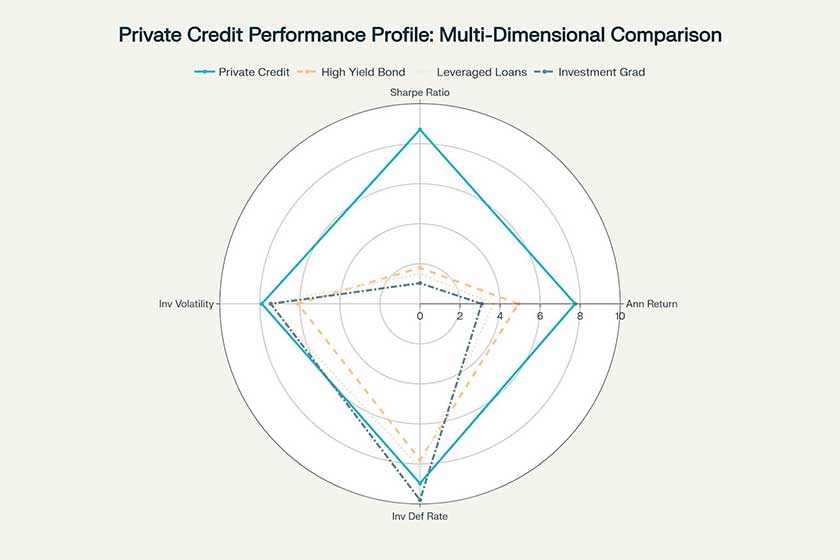

Private credit’s superior performance extends beyond simple return comparisons to encompass comprehensive risk-adjusted metrics. The asset class demonstrates exceptional consistency with 90% of years generating positive returns compared to 70% for high yield bonds.

Multi-dimensional performance comparison showing private credit’s superior risk-adjusted returns and overall investment profile across key metrics.

The maximum drawdown for private credit has been limited to -8.1% compared to -22.4% for high yield bonds and -18.2% for investment grade bonds. Recovery times following market stress have also been shorter, with private credit requiring an average of 18 months compared to 36 months for high yield bonds.

Volatility measures further support private credit’s appeal, with standard deviation of returns at 4.2% compared to 7.8% for high yield bonds and 4.9% for leveraged loans. This lower volatility, combined with higher returns, results in the superior Sharpe ratio that makes private credit particularly attractive for risk-conscious investors.

Strategic Portfolio Allocation Considerations

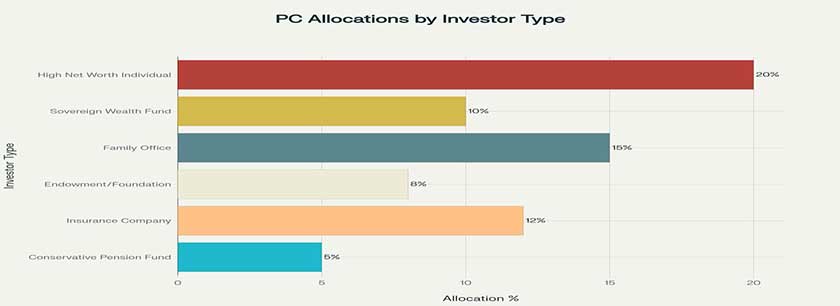

Institutional investors are increasingly incorporating private credit into their strategic asset allocations, with allocation levels varying based on investor type, risk tolerance, and liability structure. Conservative pension funds typically allocate 5% to private credit, seeking modest yield enhancement while maintaining portfolio stability.

Private Credit Allocation Percentages Across Different Types of Institutional and Individual Investors

Insurance companies, with their predictable liability streams, allocate higher percentages averaging 12%, taking advantage of private credit’s illiquidity premium to enhance spread income. Family offices and high net worth individuals often allocate 15-20% to private credit, seeking both yield enhancement and diversification from traditional investments.

The current environment presents particularly attractive opportunities for private credit investors. Private credit yields have reached a four-year high, with upper middle market private credit offering yields of 10.15% and a 226 basis point premium over B-rated loans. These attractive yield dynamics come at a time when optimism among U.S. middle market leaders is near record highs.

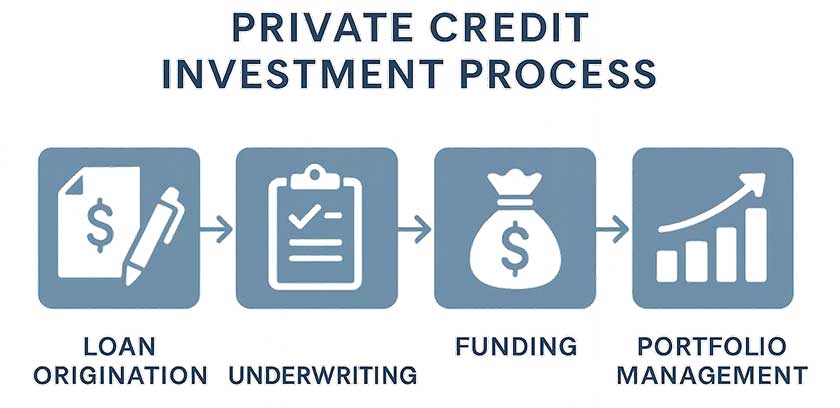

Investment Process and Due Diligence Framework

The private credit investment process involves multiple stages of analysis and risk assessment, requiring specialized expertise and resources. Private credit managers rely on established networks to source investment opportunities, typically working with private equity sponsors, investment banks, and management teams.

Unlike public markets where opportunities are broadly available, private credit requires proprietary deal flow and relationship development. Leading managers maintain dedicated origination teams that cultivate relationships with potential borrowers and intermediaries.

Sourcing and Origination

The sourcing process has become increasingly competitive as more capital flows into the asset class. According to Cliffwater, average spreads for sponsored first-lien loans ended 2024 at 524 basis points, down from 591 basis points a year ago, reflecting increased competition among lenders.

Despite spread compression, high base rates have kept yields elevated, with the Lincoln U.S. Senior Debt Index ending 2024 with a yield of 10.7% and the CDLI with a yield of 11%. This demonstrates the asset class’s ability to maintain attractive returns even in a more competitive environment.

Due Diligence and Underwriting

The due diligence process involves comprehensive analysis of borrower creditworthiness, including financial analysis, management assessment, market evaluation, and legal revie. This process typically spans 6-12 weeks and involves multiple internal stakeholders, including credit analysts, industry specialists, and legal counsel.

Key focus areas include cash flow sustainability, asset quality, management capabilities, and competitive positioning. The relationship-driven nature of private credit allows for deeper due diligence compared to public markets, resulting in better credit outcomes.

Structuring and Documentation

Private credit managers negotiate detailed loan agreements that include comprehensive covenant packages designed to protect lender interests. These covenants typically include financial maintenance requirements, reporting obligations, and restrictions on additional debt or asset sales.

The goal is to provide early warning indicators of borrower distress while maintaining operational flexibility for the borrower. This proactive approach to covenant design and monitoring is a key differentiator from public markets.

Portfolio Management and Monitoring

Active portfolio management is a critical component of private credit investing, involving ongoing monitoring of borrower performance and proactive management of distressed situations. Leading managers maintain dedicated portfolio management teams that conduct regular borrower meetings, review financial reports, and assess covenant compliance.

The ability to work directly with borrowers during periods of stress is a significant advantage of private credit, often resulting in better outcomes for both lenders and borrowers. This hands-on approach contributes to the superior recovery rates observed in private credit compared to public markets.

Fund Structure Analysis and Investment Access

Private credit funds utilize various structures to accommodate different investor preferences and regulatory requirements. The choice of fund structure depends on several factors including investor type, liquidity preferences, regulatory requirements, and fee tolerance.

Closed-end funds, which represent the majority of institutional private credit vehicles, offer limited liquidity but provide managers with stable capital for long-term lending. These funds typically charge management fees of 1.5-2.0% plus performance fees of 20% above a hurdle rate.

Business Development Companies (BDCs) provide public market access to private credit strategies, offering daily liquidity but typically with higher fee structures. The CDLI, which tracks BDC performance, has delivered strong returns with the asset-weighted index covering over 19,000 directly originated middle market loan holdings totaling $465 billion as of March 31, 2025.

Interval funds represent a middle ground, offering periodic liquidity while maintaining the ability to invest in illiquid assets. Evergreen funds have emerged as another popular structure, providing more frequent liquidity options while maintaining the benefits of private credit investing.

Insurance and Credit Enhancement Mechanisms

Private credit funds employ various credit enhancement and insurance mechanisms to mitigate risk and improve returns. These may include partial guarantees from government agencies, credit insurance policies covering specific borrower defaults, or structural enhancements such as over-collateralization.

Some funds utilize supplemental mortgage insurance (SMI) or other third-party insurance arrangements to reduce credit risk exposure. However, the effectiveness of these mechanisms depends on the creditworthiness of the insurance provider and the specific terms of the coverage.

Case Studies in Private Credit Performance

Case Study 1: COVID-19 Pandemic Resilience

During the COVID-19 pandemic, private credit demonstrated superior resilience compared to public credit markets. A leading direct lending fund experienced peak-to-trough losses of only 1.1%, significantly outperforming high yield bonds which lost 2.2% and leveraged loans which lost 1.3% during the same period.

This resilience reflected the defensive characteristics of private credit: senior secured positioning, comprehensive covenant protection, and active portfolio management. The fund’s performance during this period was supported by proactive portfolio management, including working with borrowers to implement cost reduction measures, defer non-essential capital expenditures, and access government support programs.

The floating rate structure of most loans also provided protection as rates declined, reducing borrower interest expense and improving debt service coverage. This demonstrated private credit’s ability to maintain performance even during extreme market stress.

Case Study 2: Rising Rate Environment Performance

The 2022-2023 rising rate environment provided another test of private credit’s defensive characteristics. While traditional fixed income experienced significant losses as rates increased, private credit funds generally generated positive returns due to their floating rate structures.

A representative direct lending fund generated net returns of 8.5% in 2022, compared to losses of 19% for investment grade corporate bonds and 15% for high yield bonds. This performance differential highlighted one of private credit’s key advantages: natural protection against interest rate increases through floating rate structures.

As base rates increased, borrower interest payments adjusted higher, providing immediate benefit to lenders while maintaining borrower debt service coverage within acceptable ranges. The CDLI continued to deliver strong performance throughout this period, demonstrating the asset class’s resilience across different market conditions.

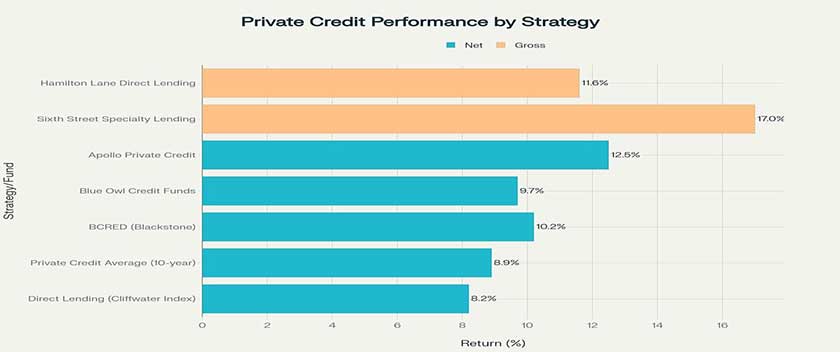

Case Study 3: Long-term Performance Track Record

Sixth Street Specialty Lending provides a compelling long-term case study in private credit performance. Since beginning operations in 2011, the fund has generated a gross IRR of 17.0% across $8.2 billion of invested capital, with 92% of exited investments producing returns of 10% or greater.

This performance reflects consistent execution across multiple market cycles, disciplined underwriting standards, and effective portfolio management. The fund’s success demonstrates the importance of experienced management teams, robust origination capabilities, and disciplined risk management in private credit investing.

Key performance drivers include maintaining strict underwriting standards, focusing on borrowers with strong competitive positions, and implementing comprehensive covenant packages to protect downside risk. The long-term track record validates private credit’s ability to generate consistent, attractive returns across varying market conditions.

Market Outlook and Future Opportunities

The private credit market outlook remains favorable, supported by structural trends in banking regulation, institutional investor demand, and borrower financing needs. Continued regulatory constraints on traditional bank lending are expected to maintain favorable supply-demand dynamics for private credit.

Basel III capital requirements and increased regulatory scrutiny of bank lending practices continue to limit traditional bank participation in middle-market lending. Meanwhile, institutional investor demand for private credit continues to grow, driven by the need for yield enhancement and portfolio diversification.

Supply-Demand Dynamics

Private equity dry powder of $1.6 trillion provides a substantial pipeline of potential financing opportunities, as these funds require debt financing for leveraged buyouts and growth capital transactions. The continued shift toward private markets and the growing sophistication of middle-market companies are expected to drive continued demand for private credit solutions.

Hamilton Lane’s analysis suggests that private credit investors are positioned to experience higher yields for longer, with 200-300 basis points of enhanced floating yield relative to the decade preceding 2022’s rising interest rate environment. The forward SOFR curve indicates rates will remain elevated compared to historical norms, supporting continued attractive yields.

Technology and Innovation

Technology adoption is expected to enhance private credit efficiency and accessibility. Advances in data analytics, artificial intelligence, and automated underwriting are enabling more efficient credit analysis and portfolio management.

These innovations may help democratize access to private credit while maintaining disciplined underwriting standards. The integration of technology into the investment process is expected to improve both origination capabilities and ongoing portfolio monitoring.

Regulatory Considerations

The regulatory environment for private credit remains generally favorable, though increased scrutiny from financial regulators may impact certain aspects of the market. The International Monetary Fund has highlighted potential systemic risks in private credit, particularly regarding interconnectedness with traditional financial institutions.

However, these concerns primarily relate to the largest funds and are unlikely to significantly impact the overall market outlook. In Europe, new rules introduced as part of amendments to the alternative investment fund managers directive (AIFMD) signal growing efforts by regulators to increase transparency, protect investors and ensure market stability.

Geographic Expansion

Private credit markets are expected to continue expanding globally, with particular opportunities in Europe and Asia. European private credit markets remain less developed than their U.S. counterparts, providing opportunities for experienced managers.

Similarly, Asian markets are beginning to develop private credit capabilities, though regulatory and cultural factors may limit near-term growth. The U.S. remains the dominant private credit market worldwide, but adoption and scaling of the asset class across Europe shows no signs of slowing down.

Risk Management and Best Practices

Effective private credit investing requires sophisticated risk management capabilities and adherence to best practices developed over multiple market cycles. Leading managers have established comprehensive frameworks that address credit risk, operational risk, and portfolio construction principles.

Portfolio Construction Principles

Leading private credit managers adhere to strict portfolio construction principles designed to optimize risk-adjusted returns. These typically include maintaining portfolio diversification across borrowers, industries, and geographies, implementing position size limits to prevent concentration risk, and maintaining adequate liquidity reserves for follow-on investments and operational needs.

The importance of diversification extends beyond simple number of holdings to include sector allocation, geographic distribution, and borrower size considerations. Heron Finance’s analysis demonstrates that true diversification requires exposure to thousands of loans across multiple fund managers and sectors.

Covenant Design and Monitoring

Comprehensive covenant packages represent a critical component of private credit risk management. These agreements should include financial maintenance covenants that provide early warning indicators of borrower distress, reporting requirements that ensure timely access to borrower information, and negative covenants that restrict borrower actions that could impair credit quality.

The proactive monitoring of covenant compliance allows private credit managers to identify potential issues early and work with borrowers to address challenges before they become material problems. This hands-on approach is a key differentiator from public markets and contributes to superior credit outcomes.

Workout and Restructuring Capabilities

Given the inherent credit risk in private credit investing, managers must maintain sophisticated workout and restructuring capabilities. This includes dedicated workout personnel, established relationships with restructuring professionals, and clear protocols for managing distressed situations.

The goal is to maximize recovery values while minimizing disruption to borrower operations. The superior recovery rates achieved in private credit (68% versus 34% for high yield bonds) demonstrate the effectiveness of these workout capabilities.

Conclusion

Private credit has established itself as a compelling asset class for institutional and sophisticated investors seeking enhanced yields, portfolio diversification, and downside protection. The asset class’s growth trajectory, supported by favorable regulatory trends and strong institutional demand, positions it for continued expansion over the coming decade.

Historical performance demonstrates private credit’s ability to generate attractive risk-adjusted returns across multiple market cycles while providing valuable diversification benefits. The defensive characteristics exhibited during the COVID-19 pandemic and 2022 rising rate environment highlight the asset class’s resilience and structural advantages.

The comprehensive analysis of returns, correlations, default rates, and risk metrics clearly demonstrates private credit’s superiority over traditional fixed income investments. With higher returns, lower volatility, better credit metrics, and superior diversification characteristics, private credit has proven itself as an essential component of modern institutional portfolios.

However, successful private credit investing requires sophisticated capabilities in origination, underwriting, portfolio management, and risk control. Investors should carefully evaluate manager experience, investment processes, and risk management frameworks before committing capital to private credit strategies.

As the asset class continues to mature and evolve, private credit is expected to play an increasingly important role in institutional investment portfolios, providing yield enhancement and diversification benefits that complement traditional asset classes. The continued growth of middle-market companies and the persistent need for customized financing solutions ensure that private credit will remain a vital component of the modern financial ecosystem.

This analysis is part of the South Sigma Insights series, providing comprehensive research and strategic analysis for business leaders and financial professionals

Have a question?

Markets Insights & Strategy

Asset Strategy Intelligence

- Annual Returns 20-50% with Zero Market Correlation: The Asset Class Wall Street Doesn’t Want You to Know About

- Evaluating External Fund Managers in 2025

- How Private Credit Funds Are Delivering 11% Returns While Bonds Struggle

- Life Settlement Funds: A Comprehensive Investment Guide for Institutional and Sophisticated Investors

Research South Sigma Disclaimer

South Sigma Consulting FZCO (“South Sigma”) is an independent investment research and advisory firm providing consulting services to advisory groups, family offices, and institutional investors. Our services include manager sourcing, strategy due diligence, and portfolio design, with a focus on alternative investments such as hedge funds, private markets, real assets, and infrastructure. The information provided by South Sigma is intended solely for sophisticated and professional investors and is for informational and discussion purposes only. It is not intended for retail investors or the general public. South Sigma does not provide financial product advice, nor does it offer, promote, or distribute specific investment products or securities. All research, opinions, and assessments are provided on a non-reliance basis and should not be interpreted as a recommendation to invest, hold, or divest from any particular fund, manager, or strategy. Users are solely responsible for verifying the information provided and conducting their own due diligence. Investment decisions should be made based on independent judgment and, where appropriate, in consultation with qualified financial, legal, and tax advisors. While South Sigma strives to ensure the accuracy and reliability of the information it provides, no warranty or representation is made as to its completeness, accuracy, or fitness for any particular purpose. The information is provided “as is,” and South Sigma disclaims all warranties, express or implied, including but not limited to warranties of merchantability and fitness for a particular purpose. South Sigma does not act as a fiduciary or agent for any party and accepts no liability for any loss arising directly or indirectly from the use of information provided in the course of its consulting services. The information is not a substitute for professional advice. All content is confidential and proprietary to South Sigma Consulting FZCO. It may not be reproduced, distributed, or published without prior written consent from South Sigma.

For inquiries, please contact info@southsigma.com.

Accept Cancel