Examining the Asset-Based Lending Landscape in the UAE: Tailoring Solutions for a Dynamic Market

Quick Stats Recap

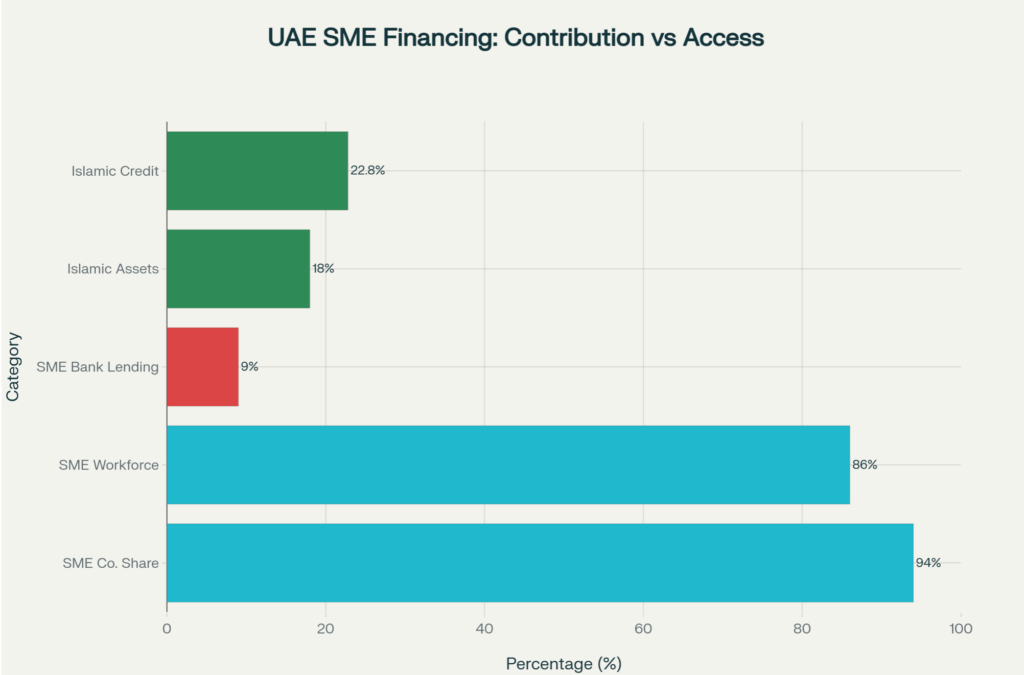

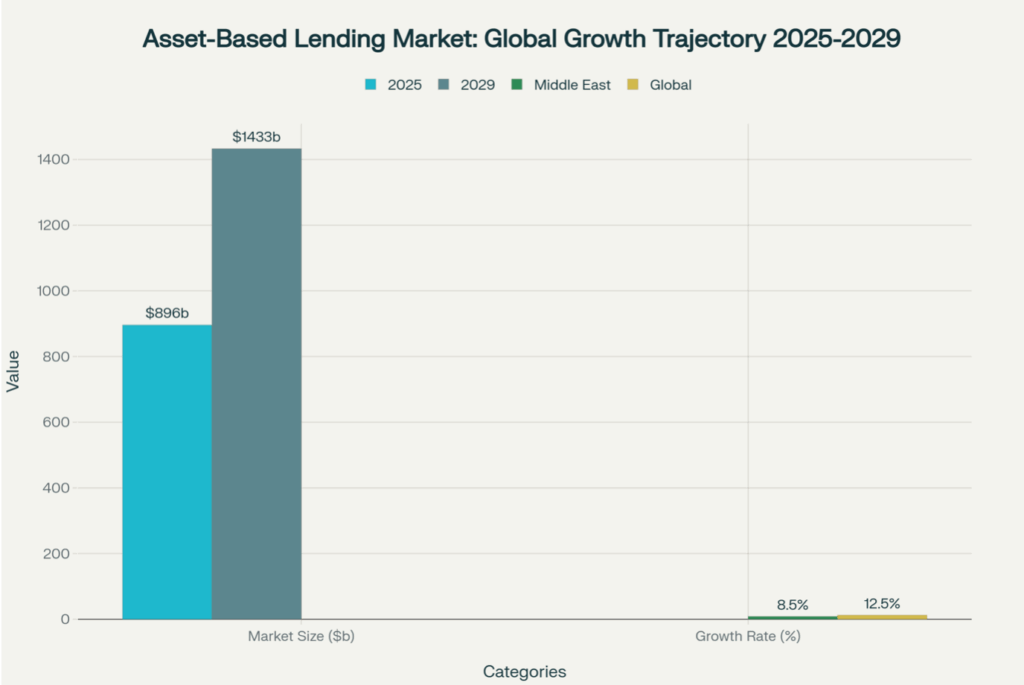

The United Arab Emirates has emerged as one of the most vibrant business hubs in the Middle East, with small and medium-sized enterprises (SMEs) forming the backbone of its diversified economy. Despite representing 94% of all registered companies and employing 86% of the private sector workforce, SMEs in the UAE face a critical financing challenge: they receive less than 10% of total bank lending. This stark disparity between economic contribution and access to capital has created significant opportunities for asset-based lending (ABL) solutions tailored to the UAE market. As the global ABL market expands from USD 896.12 billion in 2025 toward a projected USD 1.43 trillion by 2029, with the Middle East growing at 8.5% annually, understanding how to adapt ABL frameworks to local market conditions becomes increasingly crucial.

UAE SME market contribution versus access to financing, highlighting the significant gap between SME economic importance and lending allocation

The UAE’s financial landscape presents unique characteristics that distinguish it from Western markets where ABL has traditionally flourished. The country’s banking sector demonstrated robust growth in 2023, with total lending reaching AED 2 trillion (USD 542 billion), growing 6% year-over-year. Business loans grew 3.1% while personal loans surged 11.5%, indicating strong credit appetite across segments. However, the SME financing gap persists due to structural factors including perceived high risk, limited financial transparency, stringent collateral requirements, and cash flow pressures created by extended payment cycles averaging 40 days past due. Additionally, the UAE’s unique dual-banking system—with Islamic financial institutions holding 18% of total banking assets and 22.8% of total credit—requires ABL solutions that accommodate both conventional and Shariah-compliant structures.

Understanding the UAE Market Context

Economic Diversification and SME Growth

The UAE government has prioritized economic diversification away from hydrocarbon dependence, with ambitious initiatives supporting SME development as a cornerstone of this strategy. The country aims to reach one million SMEs by 2030, recognizing their critical role in innovation, job creation, and GDP contribution. This commitment manifests through initiatives like the UAE Strategy for Islamic Finance and the Halal Industry, government-backed credit guarantee schemes, and numerous accelerator programs supporting entrepreneurship across sectors including technology, manufacturing, healthcare, and renewable energy.

The construction boom across UAE metropolises drives substantial demand for imports of steel, aluminum, and cement, while exports are ramping up as diversification efforts bear fruit. Dozens of free trade zones house thousands of companies using the UAE’s strategic location to facilitate trade between Asia, Africa, and other regions, creating additional financing needs for working capital and trade transactions. This dynamic environment presents ideal conditions for ABL solutions that can provide flexible, asset-backed financing to support business growth and international trade activities.

The SME Financing Gap

Despite government support, SMEs struggle to access adequate financing through traditional banking channels. Of the AED 2 trillion in UAE bank loans, less than 10% flows to SMEs, while they constitute 94% of all companies. This financing gap exceeding USD 250 billion across the GCC region leaves thousands of growth-ready businesses undercapitalized. Several factors contribute to this challenge. Banks typically require fixed assets as security, creating barriers for newer or technology-driven firms operating with limited physical infrastructure. Even SMEs with steady revenue struggle due to opaque risk-assessment criteria and complex application procedures. Processing delays, unclear rejections, and requirements for extensive financial documentation discourage many from applying altogether.

Asset-Based Lending market size and growth projections showing strong expansion globally and in the Middle East region through 2029

The introduction of corporate tax and VAT in the UAE is gradually addressing the information asymmetry problem. Tax compliance forces creation of verifiable financial records, providing banks with the data needed to evaluate creditworthiness. However, the cash flow stranglehold from late payments persists, with 51% of all B2B invoices in the UAE paid late—higher than the Asian average—taking an average of 40 days past due to actually collect payment. This creates a vicious cycle where SMEs must either take expensive short-term credit at 14-15% fixed interest rates, delay their own supplier payments, or run dangerously thin cash reserves.

The Role of Islamic Finance

Islamic finance plays a significant role in the UAE financial ecosystem, with the country ranked as the third-largest Islamic finance market globally and fourth by total assets according to the 2023 Islamic Finance Development Indicator. The sector has grown from the establishment of Dubai Islamic Bank in 1975 to encompass multiple institutions offering Shariah-compliant banking, Takaful insurance, Sukuk issuance, and asset management. Global Islamic finance assets surpassed USD 3.88 trillion in 2024, growing 14.9% year-over-year, with Islamic banking assets expanding 17.05%. In the UAE specifically, Islamic banks account for approximately 18% of total banking assets and 22.8% of total credit.

Asset-based lending aligns naturally with Islamic finance principles, which emphasize real economic activity, asset-backed transactions, and profit-loss sharing rather than interest-based lending. Common Islamic financing structures applicable to ABL include Ijarah (leasing), Murabaha (cost-plus financing), Salam and Istisna (forward financing), and Tawarruq (commodity-based financing). The UAE Central Bank has developed specific frameworks for Islamic financial institutions to access liquidity management instruments, including purchase, repurchase, and sale of commodities and securities compliant with Shariah provisions.

Asset-Based Lending Products for the UAE Market

Receivables Financing Solutions

Receivables financing represents one of the most accessible and widely adopted ABL products in the UAE, allowing businesses to convert outstanding invoices into immediate working capital. Multiple UAE banks and specialized finance companies offer comprehensive receivables financing solutions with varying structures to accommodate different business needs.

Post-Dated Cheque (PDC) Discounting remains a cornerstone product in the UAE market, where post-dated cheques serve as common payment instruments. Banks including RAKBANK, National Bank of Fujairah (NBF), HSBC, and Commercial Bank of Dubai (CBD) offer PDC discounting facilities that provide immediate liquidity against cheques held by businesses, typically for tenors of 60-150 days. This product addresses the cash conversion cycle challenge by enabling suppliers to receive funds immediately rather than waiting for cheque maturity dates.

Invoice Discounting and Loan Against Invoices (LAI) facilities enable businesses to secure financing against outstanding invoices under open account trade arrangements. These solutions are particularly valuable for companies engaged in B2B transactions where payment terms extend beyond immediate settlement. NBF provides receivables financing with recourse for both local and overseas suppliers, with credit insurance options available to protect transaction interests. RAKBANK offers LAI facilities allowing businesses to leverage outstanding invoices as collateral for immediate funding. HSBC provides receivables finance enabling qualified clients to access up to 90% of invoice values as soon as issued, available in most major currencies and as early as the next business day.

Specialized Receivables Products address sector-specific needs. Insurance receivables financing through partnerships like Invoice Bazaar Forfaiting Services LLC provides up to 70% financing against expected payments on insurance claims, serving healthcare providers such as clinics, hospitals, and pharmacies who may not have traditional PDCs or invoices available. Progressive Payment Certificate (PPC) loans facilitate project execution by providing financing against duly authorized PPCs from well-regarded payees, easing cash flow and providing necessary liquidity for contractors.

The Emirates Development Bank (EDB) offers post-sales receivables financing as part of its comprehensive SME support, recognizing the critical importance of converting accounts receivable into immediate working capital. This complements their pre-sales purchase financing and asset-backed financing solutions designed specifically for the manufacturing, healthcare, renewables, food security, and technology sectors.

Inventory Financing Solutions

Inventory financing enables businesses to unlock cash trapped in stock, using inventory as collateral to secure working capital loans. This product category has gained significant traction in the UAE, particularly among trading companies, manufacturers, and retailers operating in sectors with longer inventory holding periods.

DMCC Tradeflow stands as one of the most sophisticated inventory financing platforms in the region, serving as a registration system for possession and ownership of commodities stored in UAE-based facilities. The platform caters to diverse financing needs with special programs for jewelry, precious stones, and precious metals, as well as Islamic financing through commodity Murabaha and Salam instruments. In 2024 alone, DMCC Tradeflow registered Islamic Finance transactions worth AED 1.38 trillion, financed AED 492 million worth of gold, and handled 8.4 million carats of diamonds. The platform incorporates state-of-the-art processes and technology to support the commodity trade sector, enhancing risk management across the entire commodity value chain with standardized legal conditions tailored to various industries.

Invoice Bazaar provides inventory finance facilities to FMCG, food commodities, and other long-expiry commodity businesses, offering working capital lines against inventory kept as collateral with logistics partner RSA Global. Clients benefit from preferential pricing on storage and logistics costs alongside credit lines for working capital and supplier payments. Typical inventory finance structures run for 60-90 days, accommodating the cash conversion cycles common in trading and distribution businesses.

GRIP Investments offers asset-based inventory financing based upon the value of pledged inventory, where inventory itself serves as loan collateral. This solution generates liquidity by unlocking cash trapped within inventory for deployment, minimizes opportunity costs from slow-moving inventory by utilizing extended holding periods to maximize borrowing capacity, and optimizes working capital cycles by enabling timely supplier settlement. Hypothecated inventory can be stored in assigned warehouses, freeing up physical storage space while providing liquidity for new purchases. The speed of execution proves particularly valuable, as eligible hypothecated inventory provides lenders with added security, facilitating swift liquidity access.

Commercial Bank of Dubai provides goods financing to unlock resources for procuring essential raw materials and inventory, offering amounts up to AED 1 million for new-to-bank clients and up to AED 1.5 million for existing clients on a short-term basis up to 12 months. This collateral-free solution features lowest-in-market interest rates, low processing fees, fast decision-making with most credit decisions within 48 hours, and repayment through equal monthly installments.

Equipment and Machinery Financing

Equipment financing enables businesses to acquire or upgrade machinery, vehicles, and technology without depleting capital reserves, with repayment terms typically aligned to equipment lifespan. The UAE market offers extensive equipment financing options serving construction, healthcare, industrial manufacturing, transportation, and technology sectors.

Emirates Development Bank provides specialized equipment financing to manufacturers needing machinery or technology to facilitate production processes. Their solutions include equipment loans for acquiring or upgrading production equipment, financing for expanding production capacity through facility upgrades or new production lines, and export activity support for businesses engaged in international trade. EDB’s sustainable vision extends to financing energy-efficient technologies and initiatives within manufacturing processes, aligned with Operation 300bn, which aims to position the UAE as a leading global industrial center by 2031. Their offerings feature flexible terms, long tenors, extended grace periods, high loan-to-value ratios, and competitive rates designed to support innovation and expansion.

Bank of Baroda UAE offers equipment and heavy vehicle finance providing up to AED 5 million for purchase of heavy-duty equipment such as cranes, forklifts, wheel loaders, excavators, motor graders, crushers, bulldozers, road rollers, ready mix carriers, and mixers. The scheme targets business concerns undertaking construction business or equipment leasing to construction companies, with loan periods up to 7 years and security through charges on purchased equipment plus personal guarantees.

RAKBANK provides machinery finance of up to AED 3 million with flexible repayment options tailored to specific SME needs, enabling businesses to invest in machinery and commercial assets for expansion. Emirates NBD offers customized financing options for both new and used commercial vehicles and construction equipment, accommodating businesses expanding operations or responding to major new contracts.

National Bank of Fujairah operates a comprehensive Equipment & Technology Supply Chain Finance division supporting companies across the entire supply chain from manufacturers to distributors. Their equipment finance services provide funding up to 100% of equipment value, preserve existing banking facilities and working capital lines, increase purchasing power, match revenue receipt to finance cost, enable fixed rate and known payments for budget simplification, and offer flexible solutions addressing mixes of new and used assets. For technology financing, NBF provides innovative working capital management solutions including receivables management maintaining liquidity through non-recourse sale of receivables, payables management enhancing payment terms and liquidity, and project finance solutions for entire IT project lifecycles.

Working Capital and Trade Finance Solutions

Working capital facilities address short-term operational funding needs, enabling businesses to manage cash flow fluctuations, cover cyclical expenses, and bridge timing gaps between receivables and payables. UAE banks offer diverse working capital products including overdrafts, short-term loans, and trade finance instruments.

National Bank of Oman UAE provides customized short-term financing solutions available for periods up to 12 months with modest collateral requirements, straightforward documentation, and dedicated overdraft accounts with active operations. Their pay-as-you-go overdraft facility helps handle short-term cash flow changes and cyclical day-to-day business expenses, targeting UAE-registered businesses operating at least 4 years with annual sales turnover exceeding AED 10 million.

First Abu Dhabi Bank participates in the Abu Dhabi Government SME Credit Guarantee scheme, providing easy financing options including working capital facilities for three-month duration and term loans up to 4 years with competitive below-market interest rates, easy documentation, and quick turnaround times. Beneficiaries include all SMEs registered as LLCs, FZEs, sole proprietorships, partnerships, and branches of foreign companies operating in Abu Dhabi engaged in trading, manufacturing, and services.

Commercial Bank of Dubai offers working capital loans including short-term loans, overdrafts, loans against progress payments, and cheque discounting, all designed to provide collateral-free access to finance with minimum formalities. Their fair pricing commitment ensures fees and profit rates remain among the lowest comparable in the UAE market, with fast decision-making and 48-hour turnaround times for most credit decisions.

RAKBANK provides comprehensive trade and working capital finance solutions through experienced Relationship Managers and their TRADEASSIST technology platform, which streamlines trade finance transactions for quick, efficient processing. Their offerings include PDC discounting to boost liquidity, loans secured by invoices as collateral, insurance receivables financing up to 70%, and guaranteed solutions including bid bonds, performance guarantees, retention guarantees, and maintenance guarantees to protect business interests.

easyCapital UAE operates as a financing intermediary connecting SMEs with banks offering working capital solutions including overdraft facilities for managing day-to-day expenses with flexible repayment and secured or unsecured options, short-term loans against purchase orders with 60-90 day tenors for bridging cash flow gaps, invoice/bill discounting with 60-150 day tenors for turning unpaid invoices into immediate cash, and letters of credit and bank guarantees for securing international and domestic trade transactions.

Islamic Asset-Based Financing

Islamic finance principles naturally align with asset-based lending, as Shariah compliance requires underlying assets for financing transactions and prohibits pure debt-based interest transactions. UAE institutions offer comprehensive Shariah-compliant ABL solutions addressing the substantial market segment preferring Islamic financial products.

Ijarah-Based Financing represents the Islamic alternative to conventional leasing, widely used for asset finance including vessel financing, equipment acquisition, and real estate. Under Ijarah contracts, the bank purchases assets which are then leased to customers for specified terms, with Ijarah wa Iqtina structures providing ownership transfer at lease conclusion. This technique proves particularly popular for longer-term asset financing where customers require eventual ownership. SAMAA Finance offers lease financing on medium and long-term basis for plant and machinery, heavy equipment, commercial vehicles, and office automation products, providing innovative asset finance solutions to over 1,200 businesses across the UAE.

Murabaha-Based Financing involves cost-plus-profit sale arrangements where banks purchase assets or commodities requested by clients and resell them at agreed markups with deferred payment terms. This structure accommodates working capital needs, inventory purchases, and trade finance requirements while maintaining Shariah compliance. DMCC Tradeflow facilitates commodity Murabaha financing for commodities stored in UAE facilities, registering AED 1.38 trillion in Islamic Finance transactions during 2024.

Salam and Istisna Financing provide forward-payment structures for agricultural products and manufactured goods respectively, enabling businesses to access working capital against future deliveries. These instruments prove particularly valuable for manufacturers and traders requiring funds for production inputs with payment linked to completed output delivery.

Tawarruq-Based Facilities utilize commodity transactions to generate liquidity while maintaining Shariah compliance, commonly employed for personal and business financing needs. Emirates NBD offers lending against secured assets as an Islamic Tawarruq-based facility, allowing customers to pledge shares or fixed deposits as collateral against financing amounts up to 95% of security value.

Emirates Islamic Bank has positioned Islamic Fintech as a key driver for harmonizing markets through Shariah-compliant digital solutions. The bank leverages AI and digital tools to deliver customer-centric savings, investment, coverage schemes, and financing products ranging from cash management and 24/7 payment solutions to trade finance and structured finance. Their approach emphasizes collaboration with fintech partners to deliver products addressing working capital, inventory, and payroll financing needs while maintaining strict Shariah compliance.

Addressing Market-Specific Challenges

Overcoming Information Asymmetry

The historical lack of financial transparency among UAE SMEs created significant information gaps preventing banks from accurately assessing creditworthiness. The introduction of VAT in 2018 and corporate tax in 2023 fundamentally altered this landscape by forcing creation of verifiable financial records. This regulatory shift provides banks with the data needed to evaluate SME credit profiles, potentially reducing the information asymmetry that kept SME lending constrained.

For ABL providers, this evolving transparency enables more sophisticated risk assessment methodologies. Rather than relying solely on historical financial statements, lenders can leverage asset valuations, inventory turnover data, accounts receivable aging reports, and equipment appraisals to make informed lending decisions. The adoption of digital lending platforms and AI tools—with 88% of lenders in 2025 using these technologies for asset valuation—improves speed and accuracy in underwriting. Blockchain adoption has reached 12% of lenders for secure, transparent collateral tracking, particularly valuable for multi-jurisdictional and syndicated deals common in the UAE’s international trade environment.

Managing Collateral Requirements

Traditional bank lending in the UAE typically requires substantial fixed assets as collateral, creating barriers for asset-light businesses, startups, and companies in technology and service sectors. Asset-based lending addresses this challenge by accepting diverse collateral types including accounts receivable, inventory, equipment, and even intellectual property in some structures.

Collateral requirements in the UAE are influenced by several factors including loan amount (higher amounts requiring higher collateral values), collateral type (lenders preferring liquid, easily valued assets), borrower creditworthiness, and sector-specific risk profiles. Common collateral forms include real estate, equipment, inventory, accounts receivable, and personal assets of business owners. The loan-to-value (LTV) ratios vary by asset class, with UAE banks typically providing 50-60% LTV for real estate-backed facilities, 60-70% for receivables financing, 50-80% for inventory depending on liquidity and shelf life, and up to 100% for equipment financing in some specialized programs.

Alternative collateral structures have emerged to serve businesses lacking traditional assets. Credit guarantees through government programs like the Abu Dhabi SME Credit Guarantee scheme enable banks to offer financing with reduced collateral requirements. Some lenders accept assignment of contracts or purchase orders as security, particularly valuable for project-based businesses. Insurance-backed receivables allow healthcare providers to access financing against insurance claims without traditional collateral.

Addressing Cash Flow and Payment Term Challenges

Late payment cycles represent a critical challenge for UAE SMEs, with 51% of B2B invoices paid late at an average of 40 days past due. This cash flow stranglehold forces SMEs to operate with thin reserves, delay supplier payments, or seek expensive short-term credit, creating a domino effect where salary delays lead to employee departures, client losses, and tightened supplier credit.

Receivables financing directly addresses this challenge by converting outstanding invoices into immediate liquidity, effectively factoring out payment delays and providing working capital for ongoing operations. Supply chain financing linked to ABL grew 10.1% in 2025, particularly in manufacturing, distribution, and wholesale trade where extended vendor terms are critical. Progressive payment certificate financing enables contractors to maintain cash flow during long-term projects by providing advances against authorized payment certificates.

DMCC Tradeflow’s approach to inventory financing helps traders and distributors manage the timing gap between inventory acquisition and final sales realization. By providing collateralized financing against stored commodities, businesses can purchase inventory, fulfill customer orders, and receive payment without depleting working capital reserves. The platform’s infrastructure ensures reliable, efficient systems for securing loans against diverse commodities from precious stones and jewelry to tea and coffee.

Embedded finance solutions are emerging as innovative approaches to the cash flow challenge. CredibleX and similar fintech platforms offer fast, flexible alternatives to traditional bank loans by integrating financing directly into business platforms and marketplaces. These solutions reduce application-to-funding timelines from weeks to days, providing timely capital access when growth opportunities arise.

Regulatory Compliance and Licensing

The UAE Central Bank regulates financial institutions through Federal Law No. 14 of 2018 (New Banking Law), which governs entities providing financing including commercial banks, investment banks, finance companies, Islamic banks, and real estate finance companies. Lenders must obtain proper licensing from the Central Bank to conduct financial arrangements with UAE borrowers, with applications requiring corporate documents, business plans, and specific documentation verified within 60 working days. Operating without appropriate licenses can result in imprisonment, fines, and liability for civil and criminal claims.

The Finance Companies Regulation updated by CBUAE Circular No. 3/2023 introduced a new category of Restricted License Finance Companies authorized to provide short-term credit (maturity less than one year) to individuals and businesses, including payday loans, overdrafts, and invoice financing. This regulatory development created clearer frameworks for fintech and alternative lenders, enhanced transparency, and improved consumer protection while enabling innovation in financing structures.

For asset-based lenders, compliance requirements include conducting periodic examinations to ensure adherence to UAE laws and regulations, submitting reports and maintaining records in prescribed formats and timeframes, obtaining Central Bank approval for changes in ownership, senior management, or capital, and implementing adequate risk management, anti-money laundering, and customer protection frameworks. The UAE’s removal from the European Commission’s list of high-risk countries for anti-money laundering in recent years reflects improved regulatory oversight systems, enhancing the country’s attractiveness for international ABL providers.

Market Opportunities and Future Outlook

Growth Drivers and Market Expansion

The UAE asset-based lending market stands positioned for substantial growth driven by multiple convergent factors. The global ABL market’s projected expansion from USD 896.12 billion in 2025 to USD 1.43 trillion by 2029 at a 12.5% CAGR reflects increasing reliance on asset-backed financing globally. The Middle East specifically demonstrates 8.5% growth in 2025, with the UAE leading regional charge particularly in oil, gas, and construction sectors.

Several market dynamics fuel this expansion. The shift toward non-bank lenders accelerates, with these institutions accounting for 34% of all ABL transactions in 2025, offering faster deal execution and more flexible structuring than traditional banks. Sustainability-linked ABL loans have grown to represent 19% of all ABL transactions as ESG compliance becomes strategic priority. The retail sector has seen 23% increase in ABL financing in 2025 as businesses respond to inventory volatility and consumer spending shifts. ABL-backed mergers and acquisitions activity rose 15.6% in 2025 as middle-market firms increasingly use asset-based structures to finance expansion, roll-ups, and distressed asset purchases.

The UAE’s trade finance market demonstrates strong momentum, with near-universal uptick in trade loan volumes, fee and commission income, and off-balance sheet trade products like letters of credit and guarantees reported by lenders. Construction of infrastructure across UAE metropolises draws imports from around the world while diversified exports ramp up, creating financing needs across supply chains. Free trade zones housing thousands of companies facilitate trade between Asia, Africa, and other regions, with banks reporting steady increases in lending supporting these flows.

Technology and Digital Transformation

Digital transformation fundamentally reshapes asset-based lending operations in the UAE. Automation in asset valuation continues reshaping ABL operations, with 88% of lenders in 2025 using digital platforms and AI tools to assess accounts receivable, inventory, and equipment values, improving speed and accuracy in underwriting. Blockchain adoption has reached 12% of lenders for secure, transparent collateral tracking, especially valuable for multi-jurisdictional and syndicated deals common in UAE’s international business environment.

Fintech platforms are making ABL more accessible to SMEs across size ranges and sectors. Emirates Islamic Bank’s Islamic Fintech initiatives leverage AI to deliver Shariah-compliant solutions for savings, investment, and financing products while maintaining ethical and purposeful cross-border compatibility. Digital KYC onboarding and e-signatures for loans have accelerated post-pandemic, making it easier for SMEs to apply for financing remotely and for lenders to assess them efficiently.

RAKBANK’s TRADEASSIST platform exemplifies technology integration in traditional banking, providing streamlined trade finance transactions with quick turnaround times through combination of dedicated relationship managers and advanced digital capabilities. Similarly, NBF’s digital platforms for receivables and equipment financing enable faster application processing and real-time facility management.

The Central Bank of the UAE’s regulatory framework developments support this digital transformation. Updated Finance Companies Regulation enables fintech businesses and licensed financial institutions to offer short-term credit through digital channels with appropriate consumer protections and transparency requirements. This regulatory clarity encourages innovation while maintaining financial stability and customer safety.

Best Practices for Implementation

Structuring Effective ABL Facilities

Successful asset-based lending implementation in the UAE requires understanding local business practices, regulatory requirements, and cultural expectations. Facilities should be structured with appropriate loan-to-value ratios reflecting asset liquidity and market conditions, typically 50-70% for receivables, 50-80% for inventory depending on type and turnover, up to 100% for equipment in specialized programs, and 40-60% for real estate-backed facilities.

Tenor selection should align with underlying asset cycles, with 60-150 days typical for receivables financing, 60-90 days for inventory financing, up to 7 years for equipment financing, and up to 12 months for working capital facilities. Repayment structures can include monthly installments for term facilities, revolving structures for working capital needs, balloon payments for project-based financing, and automatic debits from business accounts for convenience.

Security documentation must be comprehensive and legally enforceable. This includes properly executed pledge agreements for inventory and receivables, mortgage registrations for real estate collateral, equipment liens filed with appropriate authorities, and personal guarantees from business owners or directors as required. UAE’s common use of post-dated cheques as commercial instruments provides additional security mechanisms through cheque discounting structures.

Covenants should be tailored to borrower circumstances and sector norms, potentially including minimum current ratio maintenance, debt service coverage requirements, restrictions on additional borrowing, requirements for periodic financial reporting, and restrictions on asset disposition without lender consent. Islamic finance structures require additional Shariah compliance certifications and oversight by qualified Shariah scholars ensuring all transactions adhere to Islamic principles.

Risk Management and Monitoring

Effective risk management distinguishes successful ABL programs from underperforming portfolios. Initial underwriting should include thorough business evaluation examining operating history, management quality, and market position, detailed asset valuation using qualified appraisers for equipment and real estate, analysis of accounts receivable aging and customer concentration, inventory turnover analysis and obsolescence risk assessment, and sector-specific risk evaluation considering market conditions and competitive dynamics.

Ongoing monitoring proves critical for early identification of deteriorating conditions. Regular financial statement review monthly or quarterly depending on facility size, periodic asset inspections and revaluations ensuring collateral adequacy, accounts receivable aging analysis identifying concentration risks and collection issues, inventory audits verifying existence and condition of pledged stock, and covenant compliance monitoring flagging breaches requiring remediation all form essential monitoring components.

Technology enables more efficient and effective monitoring. Automated asset valuation using AI and digital platforms improves accuracy and reduces processing time. Blockchain implementations provide transparent, tamper-proof collateral tracking particularly valuable for syndicated facilities. Digital platforms enable real-time reporting and dashboard views of portfolio performance, facilitating proactive risk management.

For Islamic finance facilities, additional oversight ensures continued Shariah compliance throughout facility life. This includes regular Shariah audit reviews, documentation of underlying asset ownership and transfer, appropriate structuring of profit distributions replacing interest payments, and adherence to prohibited activity restrictions.

Building Sustainable Borrower Relationships

Long-term success in UAE asset-based lending depends on building strong, mutually beneficial relationships with SME borrowers. This relationship-based approach aligns with local business culture emphasizing personal connections and trust. Key elements include dedicated relationship managers providing personalized service and business understanding, transparent pricing and terms avoiding hidden fees or surprise charges, flexible structures accommodating business cycles and growth trajectories, educational support helping borrowers understand ABL mechanics and optimize usage, and value-added services beyond financing including advisory, networking, and business development support.

The UAE’s emphasis on entrepreneurship and innovation creates opportunities for lenders positioning themselves as true business partners rather than mere capital providers. Emirates Islamic Bank exemplifies this approach through collaboration with fintech partners to deliver solutions addressing specific SME pain points in working capital, inventory, and payroll financing. RAKBANK’s combination of relationship managers with TRADEASSIST technology demonstrates how personal service and digital efficiency can complement each other.

Government partnerships enhance credibility and access to target markets. Participation in programs like the Abu Dhabi SME Credit Guarantee scheme, collaboration with Emirates Development Bank on sector-specific initiatives, and engagement with entrepreneurship support entities and accelerators all provide channels for reaching creditworthy borrowers while benefiting from risk-sharing mechanisms.

Conclusion

The United Arab Emirates presents a compelling market for asset-based lending solutions, characterized by a large and growing SME sector facing persistent financing gaps, supportive government policies promoting entrepreneurship and economic diversification, sophisticated financial infrastructure with both conventional and Islamic banking capabilities, and strategic geographic positioning facilitating international trade. As the global ABL market expands toward USD 1.43 trillion by 2029 and the Middle East grows at 8.5% annually, the UAE stands positioned to capture substantial value by tailoring ABL solutions to local market conditions.

Success in this market requires understanding unique characteristics including the dual banking system accommodating Islamic finance preferences, the role of post-dated cheques in commercial transactions, extended payment cycles creating cash flow pressures, regulatory requirements for financial institution licensing, and cultural expectations for relationship-based banking. Providers offering comprehensive product suites spanning receivables financing, inventory financing, equipment financing, working capital facilities, and trade finance instruments, all structured in both conventional and Islamic formats, will be best positioned to capture market share.

The market’s evolution from information asymmetry toward greater transparency through tax implementation, combined with technological innovations in digital lending, AI-driven underwriting, and blockchain-based collateral tracking, creates favorable conditions for sustainable ABL market development. By addressing the critical financing gap facing 94% of UAE companies that receive less than 10% of bank lending despite employing 86% of the private workforce, asset-based lending solutions deliver economic value extending beyond individual transactions to support national objectives of diversification, innovation, and sustainable growth.

This analysis is part of the South Sigma Insights series, providing comprehensive research and strategic analysis for Accredited Investors.

Sector-Specific Opportunities

Have a question?

Markets Insights & Strategy

Asset Strategy Intelligence

- Annual Returns 20-50% with Zero Market Correlation: The Asset Class Wall Street Doesn’t Want You to Know About

- Evaluating External Fund Managers in 2025

- How Private Credit Funds Are Delivering 11% Returns While Bonds Struggle

- Life Settlement Funds: A Comprehensive Investment Guide for Institutional and Sophisticated Investors

Research South Sigma Disclaimer

South Sigma Consulting FZCO (“South Sigma”) is an independent investment research and advisory firm providing consulting services to advisory groups, family offices, and institutional investors. Our services include manager sourcing, strategy due diligence, and portfolio design, with a focus on alternative investments such as hedge funds, private markets, real assets, and infrastructure. The information provided by South Sigma is intended solely for sophisticated and professional investors and is for informational and discussion purposes only. It is not intended for retail investors or the general public. South Sigma does not provide financial product advice, nor does it offer, promote, or distribute specific investment products or securities. All research, opinions, and assessments are provided on a non-reliance basis and should not be interpreted as a recommendation to invest, hold, or divest from any particular fund, manager, or strategy. Users are solely responsible for verifying the information provided and conducting their own due diligence. Investment decisions should be made based on independent judgment and, where appropriate, in consultation with qualified financial, legal, and tax advisors. While South Sigma strives to ensure the accuracy and reliability of the information it provides, no warranty or representation is made as to its completeness, accuracy, or fitness for any particular purpose. The information is provided “as is,” and South Sigma disclaims all warranties, express or implied, including but not limited to warranties of merchantability and fitness for a particular purpose. South Sigma does not act as a fiduciary or agent for any party and accepts no liability for any loss arising directly or indirectly from the use of information provided in the course of its consulting services. The information is not a substitute for professional advice. All content is confidential and proprietary to South Sigma Consulting FZCO. It may not be reproduced, distributed, or published without prior written consent from South Sigma.

For inquiries, please contact info@southsigma.com.

Accept Cancel